There have been so many recent announcements related to 2023 adjustments, let’s just tackle them all together!

Social Security

Approximately 70 million Americans will see an 8.7% cost of living adjustment to their Social Security benefit and SSI payments come 2023. “On average, Social Security benefits will increase by more than $140 per month starting in January,” says Jeff Nesbit, Deputy Commissioner for Communications at Social Security.

On the flip side, more of worker’s income will be taxed to help pay into the Social Security and Medicare programs. The same 7.65% tax rate applies to W-2 employees (x2 for self-employed), but up to $160,200 of wage will be taxed vs a max of $147,000 in 2022.

Another amount worth mentioning is the income threshold applicable to those taking Social Security prior to reaching full retirement age (FRA). In 2023, if earning more than $21,240/yr while taking Social Security “early” will result in $1 of benefits withheld for every $2 in earnings above the $21,240 limit.

Here is Social Security’s full fact sheet for all changes.

Medicare

Not seen in over a decade, Medicare Part B Premiums have DECREASED. The base monthly premium for Medicare Part B enrollees will be $164.90 for 2023, a decrease of $5.20 in 2022. The annual deductible for all Medicare Part B beneficiaries is $226 in 2023, a decrease of $7.

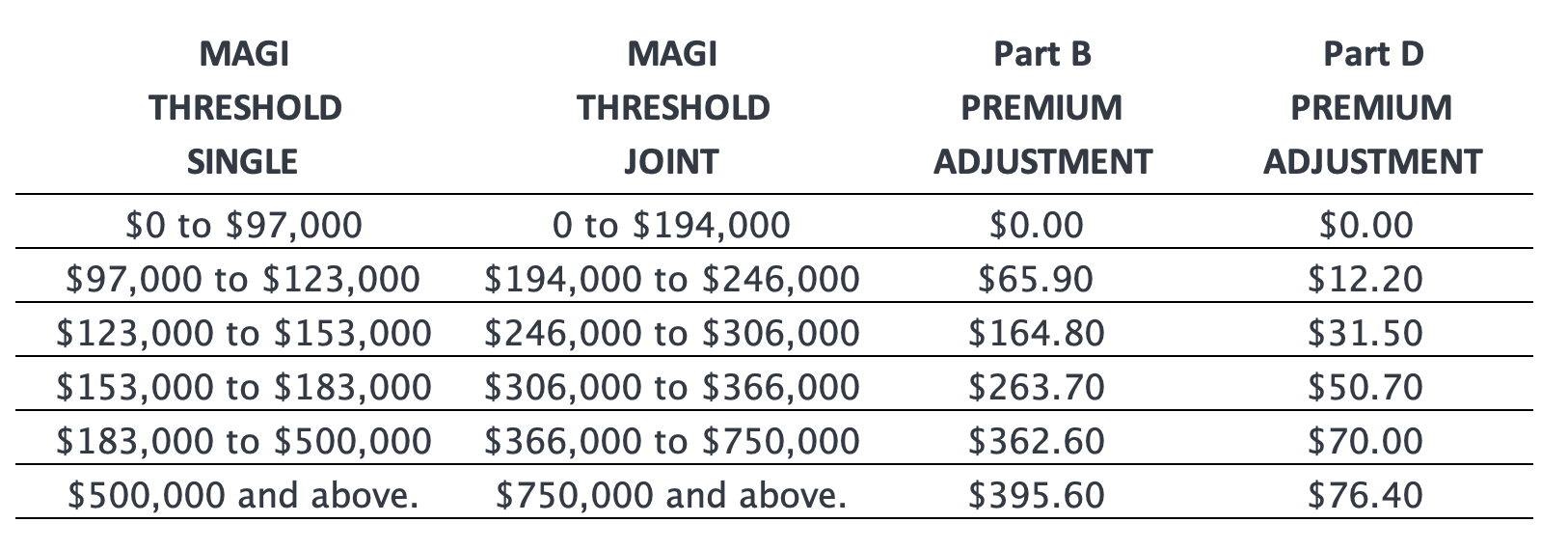

Medicare premiums are adjusted based on income, meaning higher income enrollees pay $164.90 for Part B and about $31.50 for Part D PLUS the adjustment. Brackets and adjustments for 2023 are shown in attached chart *click to enlarge*.

You may also notice a new premium table that may or may not apply to you. Beginning in 2023, certain Medicare enrollees who are 36 months post kidney transplant, and therefore are no longer eligible for full Medicare coverage, can elect to continue Part B coverage of immunosuppressive drugs by paying a premium. For 2023, the immunosuppressive drug premium is $97.10. For more information on this specifically, read on here.

The Medicare Part A has no premium to the extent you qualify by having 40-quarters of eligible work history. That said, there are deductibles and co-insurance amounts that increased from 2022. For instance, if admitted to the hospital, there is a $1,600 deductible in 2023, an increase of $44. This deductible covers costs for the first 60 days of Medicare-covered inpatient hospital care in a benefit period.

In 2023, beneficiaries must pay a coinsurance amount of $400 per day for the 61st through 90th day of hospitalization in a benefit period and $800 per day for lifetime reserve days (you receive 60 of these in your lifetime). Benefit periods are not based on a calendar year, they reset when no services are received for 60 days.

For beneficiaries in skilled nursing facilities, the daily coinsurance for days 21 through 100 of extended care services in a benefit period will be $200.00.

In terms of coverage, a big win in 2023 was related to prescriptions. The cost of insulin will be capped at $35 for a 30-day supply, and most vaccines will be free. This includes the popular shingles vaccine. More changes are slated for 2024 and 2025 related to capping out-of-pocket costs entirely and limiting premium increases. While mostly good news, the max Part D deductible edged up slightly, and is now $505/year.

Inherited IRAs

The SECURE Act changed distribution rules related to inherited IRAs. Starting 2020, non-spouse beneficiaries would need to distribute inherited IRAs within 10-yrs. It was unclear whether the IRAs needed to be taken out evenly, as desired, or even as a single lump in year 10.

The IRS has just recently provided clarity on the topic although more needs to be ironed out. If RMDs had never been started by the original owner, there is flexibility for how the distribution occurs over the 10-yr period. But if they had started, it’s expected that distributions are taken according to an RMD table in years 1-9, and fully cleared out in year 10. If this wasn’t done in 2020 and 2021 due to confusion on the matter, there will be no penalty. But it’s expected to be understood in time for 2022.

Use this handy calculator to help determine your RMD for 2022.

Income Tax Brackets

The favorable changes made via the Tax Cuts and Jobs Act are set to sunset after 2025. Until then we may not see any material changes apart from normal inflation adjustments to the brackets. See chart for updated brackets, no changes to the rates. *Click to enlarge.*

The standard deduction for single taxpayers in 2023 will rise by $900 to $13,850, and increase for married taxpayers filing joint returns by $1,800 to $27,700.

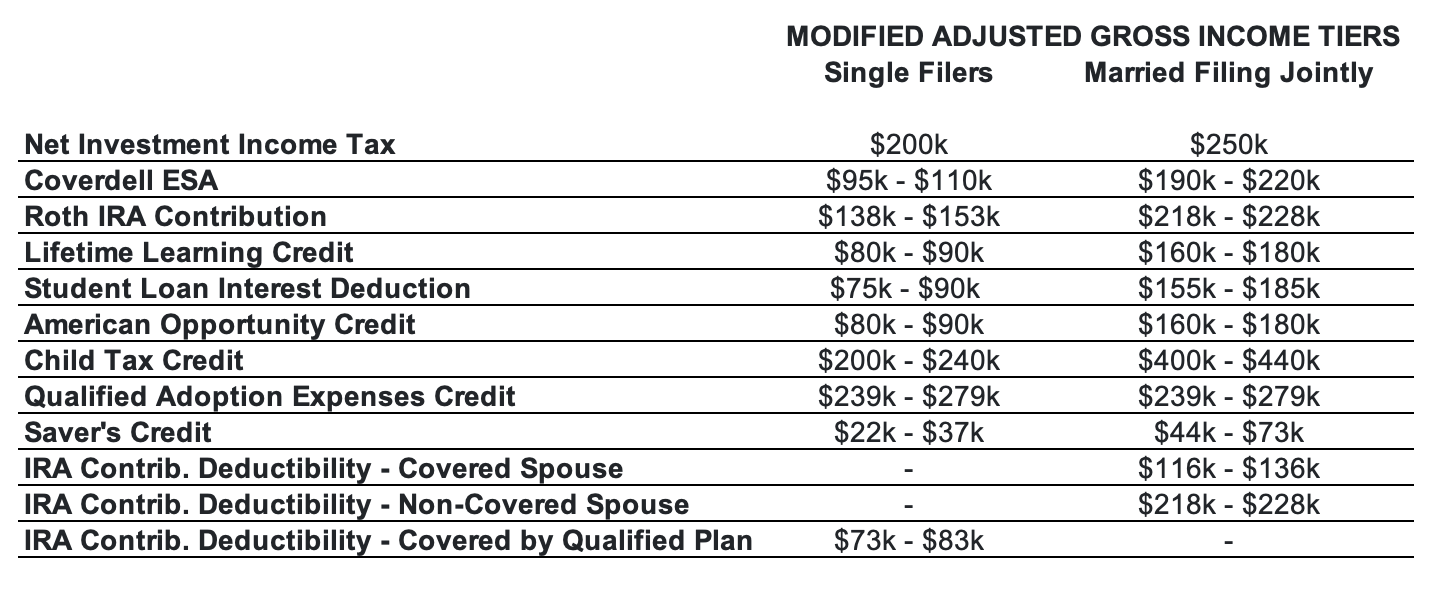

As it relates to the finer points of a tax return, ie – various deductions and credits, see the following chart. Unfortunately, there has been no adjustment to the Net Investment Income Tax or the Child Tax Credit thresholds – that would have been nice! If interested in information related to deductions and credits for clean energy, read my blog on How to Capitalize on the Inflation Reduction Act of 2022.

Click here for the full announcement related to income tax adjustments.

Retirement Plan Contribution Limits

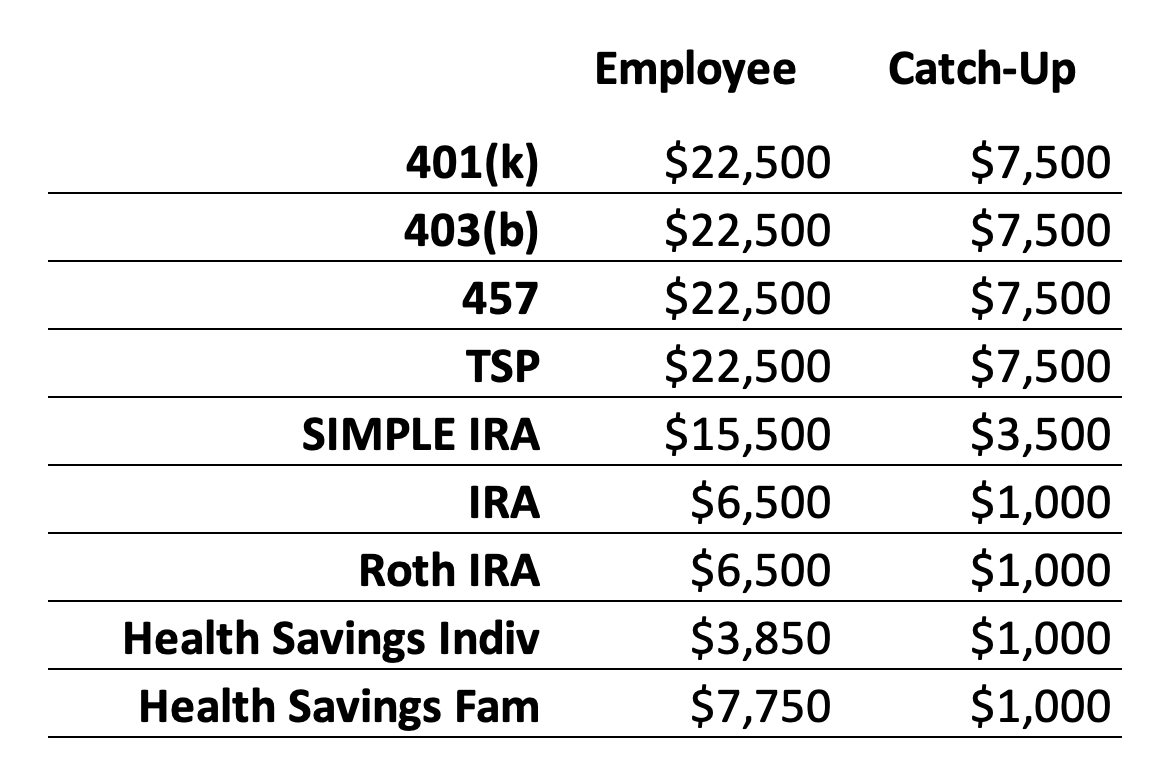

Employee benefit packages are starting to roll out, and you may be asked to make or confirm contribution elections toward retirement plans and health savings accounts. There are increases across the board in 2023 for how much can be contributed. See our chart for the most popular plans. *Click to enlarge.*

Employee benefit packages are starting to roll out, and you may be asked to make or confirm contribution elections toward retirement plans and health savings accounts. There are increases across the board in 2023 for how much can be contributed. See our chart for the most popular plans. *Click to enlarge.*

IRS Release on increased limits.

Gifting

Lastly, the annual exclusion gift limit has increased to $17,000. This means any one person can give any other person up to \$17,000 without having to file a gift tax return. IE) A married couple could give each of their children $34,000/year.

If you’re looking to reduce your estate, making annual gifts can really add up over time. That said, the federal lifetime gifting exemption will be $12,920,000 per person. What does this mean? Any person can gift $12,920,000 over their lifetime and avoid the gift tax of 40%. For example, let’s say you give a child $100,000 toward a house downpayment that exceeds the $17,000 annual exclusion. It’s not a taxable problem, it’s just now reportable via a gift tax return. Once reported, you’ve knocked off $100,000 from your $12,920,000 lifetime exemption. For the vast majority, exceeding the federal lifetime limit will never be a problem.

Keep in mind though, various states including MA impose their own “death tax.” In MA, state estate tax triggers at the $1,000,000 mark. So taking full advantage of annual exclusion gifts can make a lot of sense.