A rise in mortgage rates does impact borrowing costs and borrowing abilities and housing will absolutely feel the effect. By how much is anyone’s guess and more a function of location and supply.

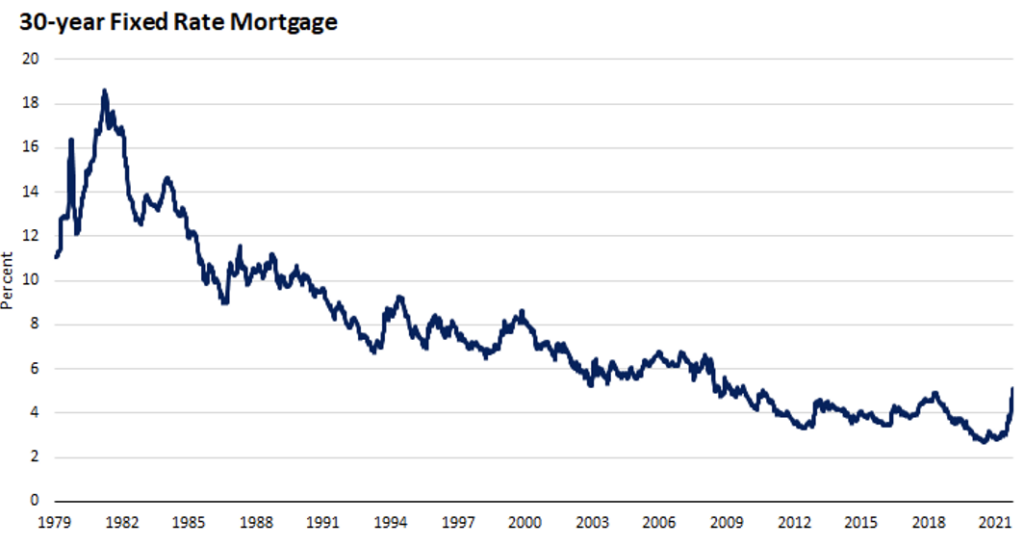

On top of everyone’s mind is the fact that the average 30-year fixed-rate mortgage moved above 5% from 3% six months ago. But it’s worth noting that mortgage rates hit 5% in 2011 and 2018 – and averaged over 7% from 1990 to 2010.

However, would-be-buyers tend to remember recent history and mortgage rates have been very low for a long time. In fact, mortgage rates have averaged 3.7% from 2016-2021 and 3.0% over the last two years.

But think about this: The median existing-home price for all housing types in March was $375,300, up 15.0% from March 2021 ($326,300). This marks 121 consecutive months of year-over-year increases, the longest-running streak on record. That’s more than 12-years.