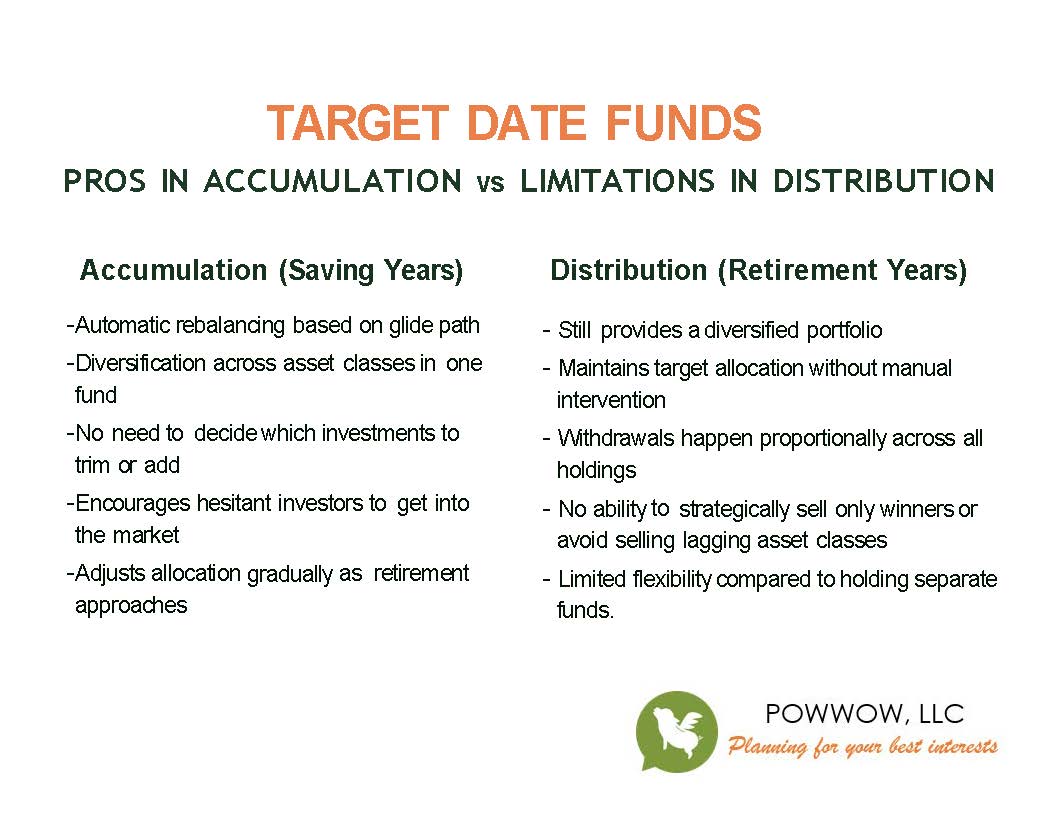

Target date funds have done a world of good for retirement investors, especially those who may have been hesitant to start. Target date funds simplify investing, encourage participation in the markets, and take advantage of long-term compounding without requiring the investor to constantly rebalance or strategize.

I’m a fan, particularly in the accumulation phase. But I also think they have limitations once retirement begins. Here’s my take on when they shine and when you might want to consider alternatives.

Why Target Date Funds Work Well in the Accumulation Phase

During your working years, it’s likely not necessary to hold a large collection of funds for strategic purposes. A target date fund manages the asset allocation for you, rebalancing periodically based on the fund’s glide path.

What target date fund managers review when rebalancing:

-

Market conditions and economic trends — Adjustments may be made based on interest rates, inflation, or recession risk.

-

Asset class performance — The fund might rebalance between equities, bonds, and other asset classes to maintain the intended risk level.

-

Glide path progression — As the “target date” approaches, the allocation gradually shifts from aggressive (more equities) to conservative (more bonds and cash equivalents).

-

Longevity and withdrawal assumptions — Managers model how much risk is appropriate given expected retirement length and spending patterns.

For investors not yet taking withdrawals, the fund automatically maintains balance and diversification. You don’t have to decide which holdings to trim, because you’re not generating cash flow—you’re simply investing for growth.

Why I’m Cautious About Target Date Funds during Retirement

Once retirement begins and periodic withdrawals (or required minimum distributions) start, things change. A target date fund still holds the same diversification, but you lose the ability to be strategic about which parts of your portfolio you tap for cash.

For example:

-

If international stocks are underperforming, you may want to avoid selling them while they’re down—letting them recover instead.

-

If U.S. equities are riding a hot streak, you might choose to sell some of those gains before a potential pullback.

-

If bonds are having a bad run due to interest rate hikes, you might prefer to pull from equities temporarily.

With a portfolio built from separate asset class funds, you can make those calls. A target date fund bundles it all together, so withdrawals happen proportionately, no matter the market environment.

Choosing the Right Target Date Fund

Here’s where I think many investors get tripped up: the “date” in the fund’s name is less important than the allocation inside it.

Target date funds often shift from aggressive to conservative in a short window of time. That might not match your risk tolerance or retirement timeline.

Examples:

-

If you’re young — The “right” date based on your age could have you 90–100% in equities. But if that’s too aggressive for your comfort, you could choose a fund with a nearer target date for a more balanced mix.

-

If you plan to work longer — Let’s say you’re 65 but still working for 10 more years. Your age-based target date fund might already have you in a 50/50 allocation. If you’re comfortable with more risk, you could choose a fund with a later date to increase your equity allocation to something more appropriate.

Tip: Be sure to look at the actual asset allocation, not just the year in the fund’s name. And revisit annually to ensure you’re not surprised by any glide path shifts.