Over the last handful of years I’ve received many notices from clients related to LTCi premium hikes. Due to underwriters totally missing the mark on pricing policies when they first became available (and for years thereafter) – insurers are petitioning states to approve premium increases to stay solvent. They’ve also completely discontinued certain coverage options entirely. Below is an actual example of a policy I recently reviewed:

Dear Ms. Johnson,

“If we don’t hear from you by the specified date, this 94.995% rate increase will take effect on your current coverage. If you are comfortable reducing your benefits, the alternatives below are designed to provide different levels of cost and coverage as you evaluate your current needs.”

So the question becomes – should you accept the increase or an alternative?

Remember, they totally botched the pricing on these policies, so accepting one of the alternatives most certainly would mean trading in a meaningful amount of coverage, aka value, to rectify the mistake. I’ve rarely (if ever), have found the trade-off in premium savings to be anywhere close to the coverage sacrificed.

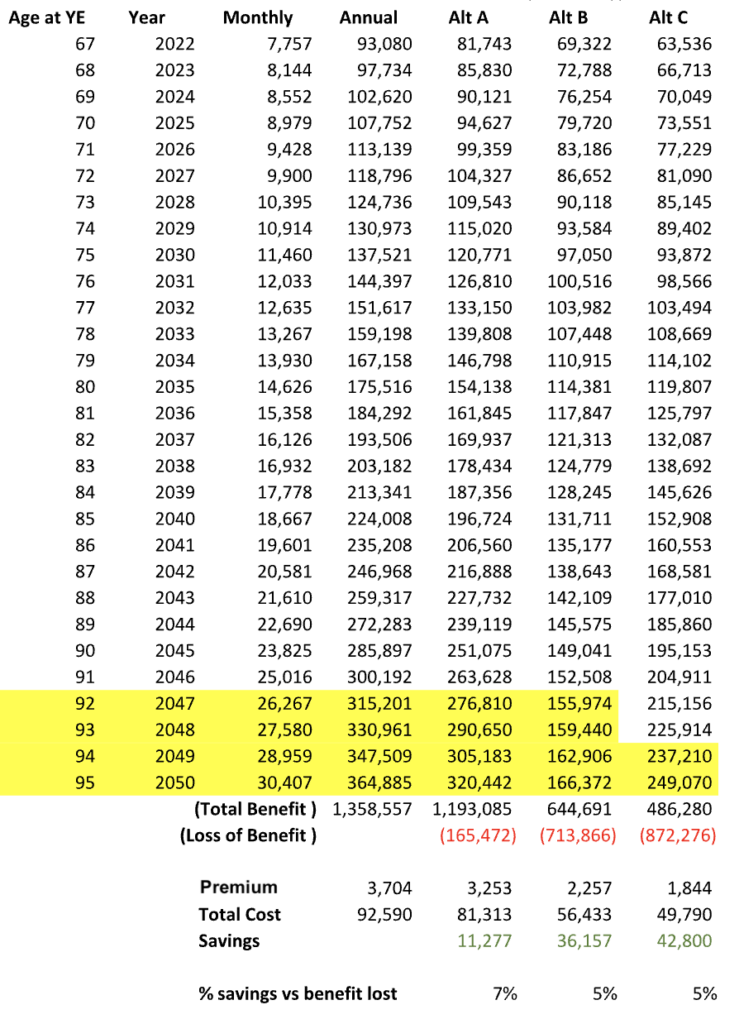

Let me break down the offer to keep the policy as-is:

- Premium: $1,899.28/yr → $3,703.56/yr (94.995% increase)

- Benefit: $7,756.65/mo

- Benefit Period: 4 years

- Annual Increase: Compound 5%

- Elimination period: 90 days

Here are the offered alternatives to make the premium increase more palatable:

Alternative A: Reduce monthly benefit to $6,611.89 with a premium increase to $3,252.50

Alternative B: Reduce monthly benefit to $5,776.80 and annual benefit increases at a simple 5% rate vs compound rate. Premium increase to $2,257.32.

Alternative C: Reduce monthly benefit to $5,294.69 and receive benefits for 2 years rather than 4. Premium remains similar at $1,844.06.

This person is age 67. And most policies, including this one, have a rider that allows the insured to stop paying premiums once the policy is triggered. Assuming they live until age 95, they would trigger the policy at age 91 (since it’s a 4 year benefit) in all scenarios other than Alternative C (only a 2 year benefit).

In all cases, relative to what you save in premium compared to leaving the policy as-is and accepting the full hike, there is a very material sacrifice of benefits in exchange. Alt C is the worst offender despite it being the most appealing for premium savings. With our assumptions, $42,800 could be saved in premium but $872,276 in benefits sacrificed. Ouch!

And when I ask my trusted LTC insurance broker, Meredith Pensack, on her thoughts about premium increases, she’s armed with the numbers.

“The statistical likelihood of needing assistance is 1 in 3 for males and 1 in 2 for females. This is a sobering reality! The number of people expected to be diagnosed with a severe cognitive impairment or Alzheimer’s disease in the coming years is predicted to increase dramatically. Nearly 10 million people worldwide are diagnosed with dementia each year, joining the 55 million others who already have this devastating condition.

The US government estimates that couples need to have $250,000 to cover future health care costs that aren’t covered by insurance. My suggestion is that if an increased premium is affordable, the policyholder should accept the increase and re-evaluate again in the future, knowing that it can be reduced at any point if necessary.”

The case for accepting alternative coverage

There are a couple cases where it might make sense to accept one of the alternatives. The first is that the coverage was purchased as a safety net prior to retirement. But now that you’re retired and more sure of your finances, you may feel the policy isn’t needed to cover your care. Additionally, if you’re not concerned about preserving net worth for the next generation or other endeavors, then paying top dollar for the most amount of coverage can feel unnecessary.

You may also feel like the benefit has compounded to an amount that well exceeds the cost of preferred care. Especially when you add in other sources of income, like social security and pensions. Maybe you feel over-insured and this is an opportunity to make an adjustment. I’ll say here though, that you can start distributions for a lesser amount to cover costs which simply extends the benefit. It’s not use it or lose it.

To explain this further, let’s say your benefit has grown to $10,000/mo for 4 years, but your preferred assisted living is only $7,000/mo. You don’t lose the $3,000 difference. It just extends the term of the policy, meaning in year 5 you’ll have a balance on the policy that you can continue to draw from. So while the benefit for any one year may seem more than you’ll need, you can also consider it as a way to afford private pay care for a longer period of time.

The second reason to elect an alternative is you truly can’t afford the premium increase. This is completely understandable. In this case, you’re somewhat painted into a corner on having to accept one of the alternatives, but it’s better than canceling. In this case, stopping payment would provide you with a paid up certificate of $17,093 toward future care needs. If you can only manage the existing premium, then the answer is pretty obvious (Alt C). But take heart knowing that in Massachusetts, because the Alt C policy still meets the 2 year benefit term and exceeds $125/day, you retain certain protections on your home for owning the policy should Medicaid ever come to pass.

Lastly, Meredith, has a suggestion for alternative coverage as well that wasn’t included in my most recent review:

“Assuming that the policyholder’s health is still good, a hybrid LTC insurance policy is an option that could be explored. This type of policy has a guaranteed premium (can never increase) and returns a tax-free death benefit if care isn’t needed.”

She goes on to let us know that, “If the rate increase letter did not include any options, or if the policyholder would like to see more options, they should contact the insurance company’s Customer Service Department to request a variety of choices at different reduced premium levels. Policyholders need to understand that regardless of rate increases, they can always reduce their benefits and premium in the future. However, once benefits are reduced, they cannot be increased.”