A CFP®’s Guide to Comparing Trump Accounts, 529 Plans, UTMAs, and IRAs

The new Trump Account for children has generated a lot of buzz-including a free $1,000 government contribution for eligible newborns. But how does it really compare to the accounts families have been using for years?

Here’s an objective, side-by-side look at how Trump Accounts work, how they compare to 529 plans and UTMAs, and when opening one might (or might not) make sense for your family.

Why All the Headlines?

Every eligible newborn receives a one-time $1,000 federal contribution. That’s the reason to open one right there.

Some children born before 2025 who are age 10 or younger and live in lower-income areas may also qualify for separate charitable deposits, such as a $250 deposit from the Dell Foundation. This is a separate initiative from the federal program. That’s why you see the Dell family frequently mentioned in Trump Account headlines.

How a Trump Account Works

Contributions are made with after-tax dollars. The money grows tax-deferred, and when distributions are taken in adulthood:

- Your original contributions come out tax-free.

- Investment earnings are taxed as ordinary income, just like a traditional IRA.

This makes the account most similar to a non-deductible IRA (in my opinion). And personally, when these come across my desk I make an audible “agh!” Only because clients often haven’t tracked post-tax contributions, making the potential to double tax those dollars fairly high. That said, Trump accounts end when the child turns 18 and the Trump Account app should have done all the necessary tracking over the years to let you now what portion of the account is contributions (post-tax) and what is tax-deferred earnings. At age 18, the account can then roll over to both an IRA and Roth IRA. That ends the need to track.

Funds generally cannot be withdrawn until the year the beneficiary turns 18. After that, the account behaves much like an IRA, including early withdrawal rules and the potential 10% penalty.

| Exception | 10% Penalty Waived? | Ordinary Income Tax Still Applies? |

|---|---|---|

| Qualified higher education expenses | ✓ | Yes |

| First-time home purchase (up to applicable limit) | ✓ | Yes |

| Disability | ✓ | Yes |

| Death (beneficiary distributions) | ✓ | Yes |

| Certain substantially equal periodic payments (SEPP) | ✓ | Yes |

| Certain unreimbursed medical expenses (subject to IRS rules) | ✓ | Yes |

| Health insurance during unemployment (if applicable under IRA-style rules) | ✓ | Yes |

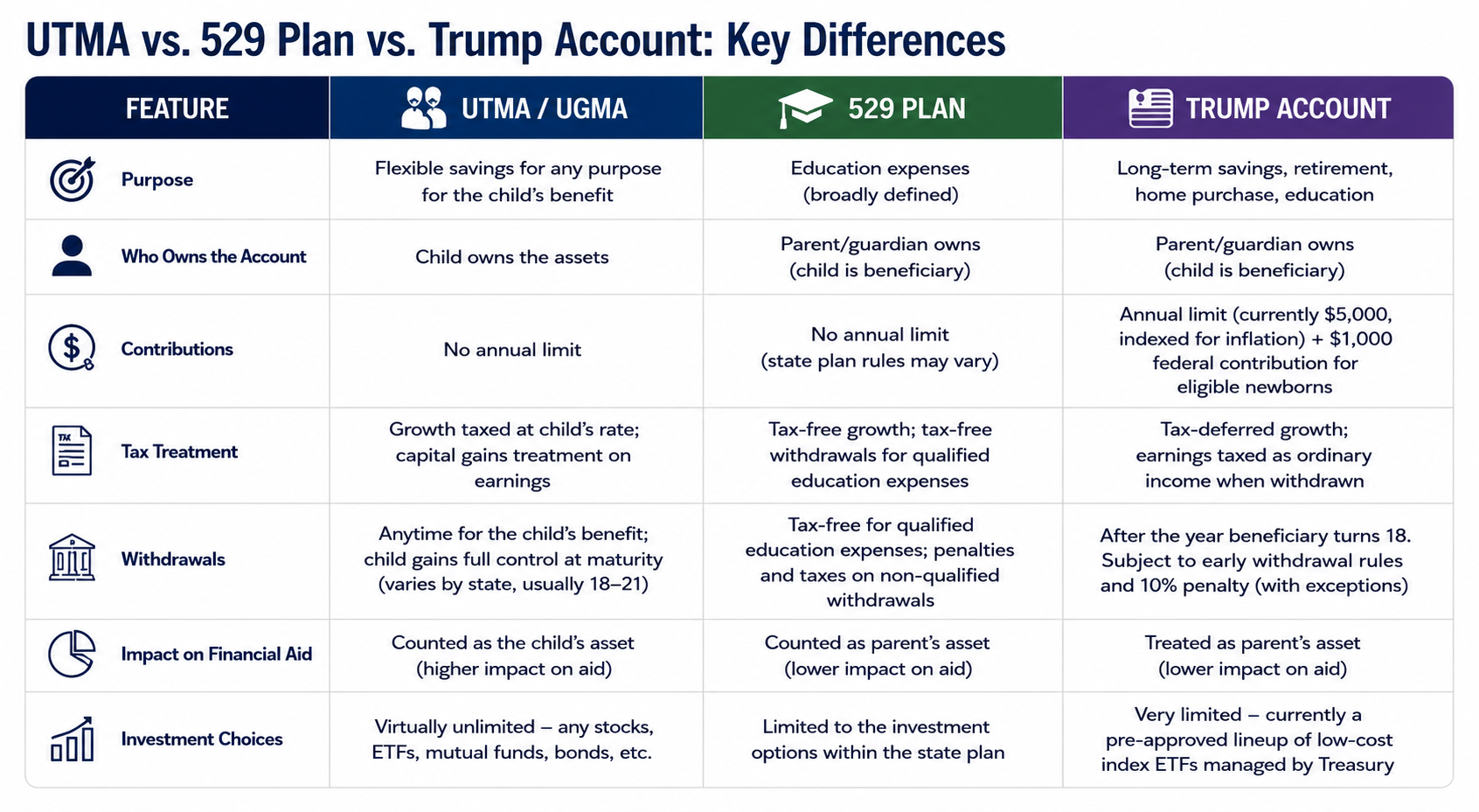

Key Differences between Savings Options

As noted, the Trump Account isn’t the only way to save for a child. There are already a number of child-related saving vehicles in place. Whether you’re setting aside birthday money, a cash gift from grandparents, or building a long-term nest egg, each account has its own strengths and tradeoffs. The chart below highlights the key differences between the three most common investment options. If you’re looking for a broader discussion on where to invest a cash gift—including trusts, Roth IRAs, CDs, savings bonds, and even good old-fashioned piggy banks, be sure to read my companion guide, Where Should You Put a Cash Gift for a Child?

A Retirement Account for Kids?

One of the most interesting aspects of the Trump Account is that it gives children access to something that functions similarly to a retirement account without requiring earned income.

Normally, children need earned income before they can contribute to a Roth IRA or traditional IRA. While some families accomplish this through a family business or other arrangement, it’s not practical for most. Annual contributions to an IRA are also limited ($7,500 in 2026), which makes adding $5,000 to a Trump account an overall easier and fairly comparable route.

For high-net-worth families who have already maxed out their own retirement accounts and funded education goals, the Trump Account can be a powerful way to give a child a jump start on retirement, or help them save for a first home down payment.

The Bottom Line

The Trump Account isn’t a replacement for 529 plans or UTMAs. But for many families, especially those who want to help a child build long-term wealth or retirement savings, it can be a valuable addition to the overall plan. As always, the best account is the one that best matches your family’s goals and tax situation.

Order to consider:

- Capture the free $1,000 federal contribution for newborns while available.

- Take advantage of any employer matching contributions if available.

- Focus on funding educational goals through a 529 plan.

- Consider a UTMA if flexibility is important.

- For families with additional savings beyond those priorities, the Trump Account can be a smart way to jump-start retirement savings.

How to Open a Trump Account

Opening a Trump Account is straightforward:

- Visit TrumpAccounts.gov.

- Download the official Trump Accounts app.

- Sign in using your IRS account (ID.me verification).

- Complete IRS Form 4547 electronically to establish the account and, if eligible, claim the $1,000 federal contribution. This can also be mailed in.

- Once approved, select your investments and begin making optional contributions.