Many parents are preparing to send children off to school this fall. While the checklists grow and the kids soak in the last few minutes of summer break, it’s important to remember the tuition fee schedule and back-to-school shopping may be more expensive this year.

And while getting through the curriculum itself can feel overwhelming, paying for it can seem nearly impossible. And living in New England means I’m not just approached with helping families plan for college, but private K-12. So the cost of tuition and everything directly related to school – think books, room and board, fees, and transportation – can certainly exceed well beyond 4 years of college.

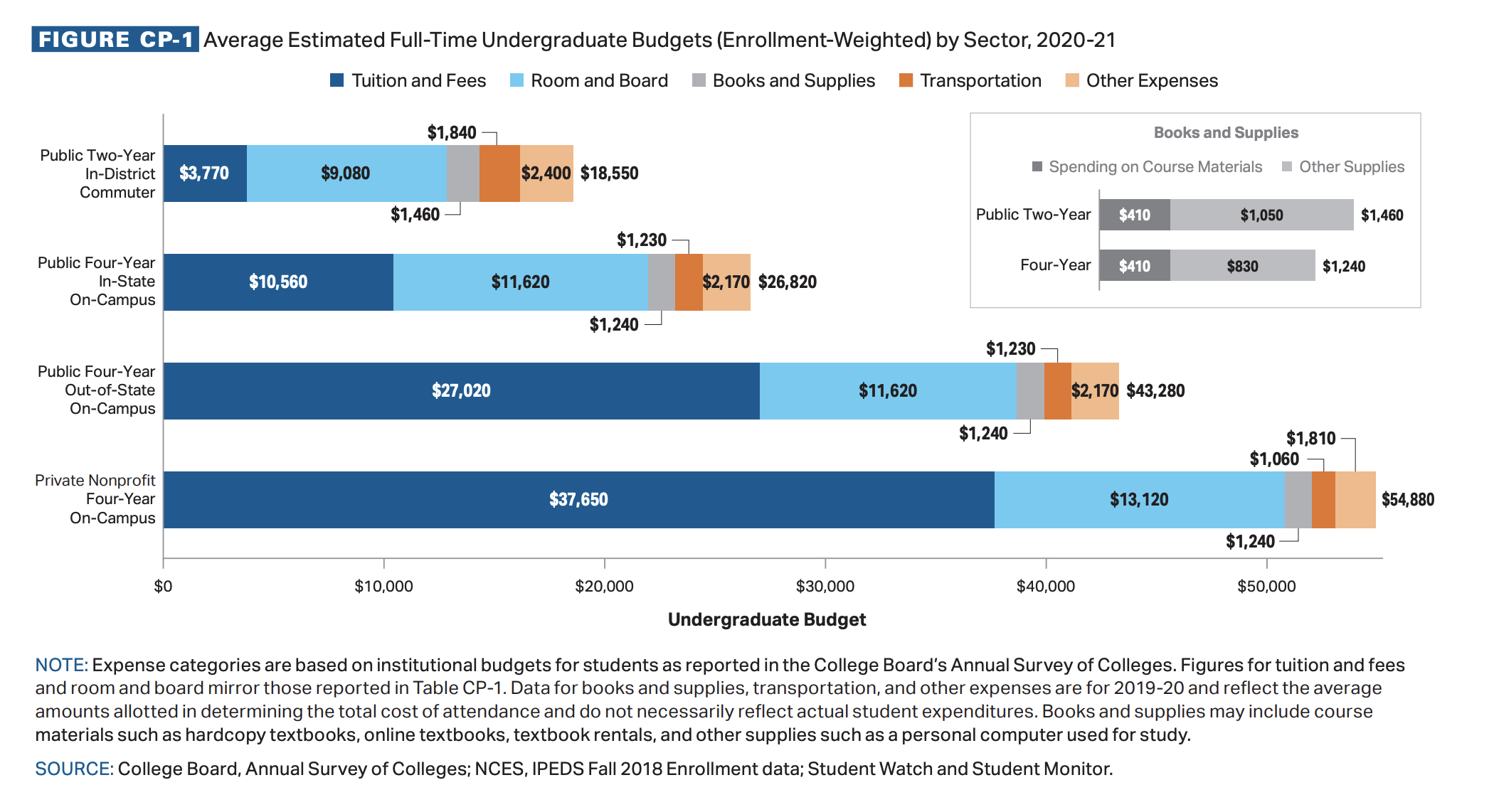

So what are costs looking like for 2021? For example, average expenses related to college for the 2020-21 academic (pandemic) year increased to $26,820 for in-state students at four-year public colleges, according to the College Board. And the same expenses at four-year private institutions rose to $54,880. With the Delta variant spreading and CPI inflation, the 2021-22 school year is set to be that much worse. See the full breakout for last year below: